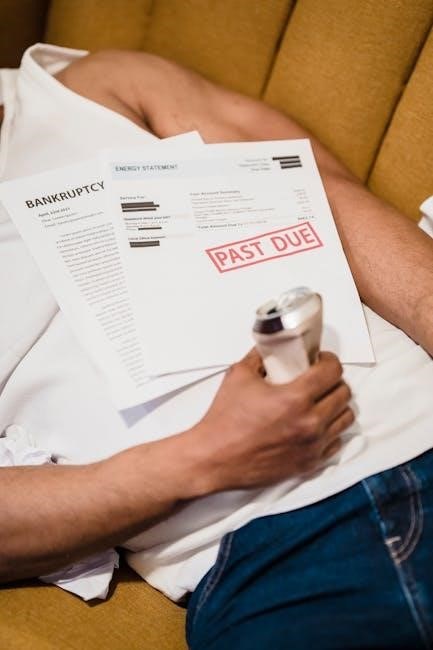

the debt snowball worksheet answers pdf

The Debt Snowball Method is a popular strategy for paying off debt, emphasizing quick wins by tackling smaller balances first to build momentum and motivation.

1.1 What is the Debt Snowball Method?

The Debt Snowball Method is a debt repayment strategy where individuals pay off debts starting with the smallest balances first, while making minimum payments on larger ones. This approach, popularized by financial experts like Dave Ramsey, focuses on achieving quick wins to build momentum and motivation. It often involves using tools like the Debt Snowball Worksheet to organize and track progress effectively.

1.2 Origin and Popularity of the Debt Snowball Strategy

The Debt Snowball Strategy gained prominence through financial expert Dave Ramsey, who championed its effectiveness in his books and media. Its popularity stems from its psychological benefits, providing quick wins that motivate individuals to continue debt repayment. The strategy has become a cornerstone of personal finance, widely adopted due to its simplicity and the encouraging results it delivers to users.

Understanding the Debt Snowball Worksheet

The Debt Snowball Worksheet is a tool designed to help individuals organize and track their debts, prioritizing them by payoff balance to accelerate repayment progress.

2.1 Overview of the Debt Snowball Worksheet

The Debt Snowball Worksheet provides a structured format for listing debts, calculating interest rates, and tracking monthly payments. It helps users prioritize debts by payoff balance, enabling a clear plan for debt elimination. By organizing financial data, it simplifies the debt repayment process, making it easier to stay focused and motivated throughout the journey.

2.2 Key Components of the Debt Snowball PDF

The Debt Snowball PDF typically includes sections for listing debts by balance, calculating interest rates, and tracking progress. It often features columns for monthly payments, total interest, and payoff dates, providing a comprehensive view of financial obligations. Additional tools like budgeting templates and milestone trackers enhance its effectiveness, helping users maintain discipline and clarity as they work toward becoming debt-free.

Benefits of Using the Debt Snowball Worksheet

The Debt Snowball Worksheet offers clear financial tracking, helping users prioritize payments and stay motivated. It provides a structured approach to debt repayment, enhancing discipline and clarity.

3.1 Psychological Advantages of the Debt Snowball Method

The Debt Snowball Method provides immediate psychological benefits by quickly eliminating smaller debts, boosting confidence and motivation. This approach creates a sense of accomplishment, encouraging individuals to stay committed to their debt repayment journey. The visible progress helps reduce stress and fosters a positive mindset, making the process feel more manageable and rewarding over time.

3.2 Financial Benefits of Using the Worksheet

The Debt Snowball Worksheet offers clear financial benefits by helping users pay off debts faster and reduce interest accumulation. It organizes payments, prioritizes balances, and provides a structured plan to eliminate debt efficiently. By focusing on smaller balances first, individuals save money on interest over time, achieving financial freedom more quickly and effectively.

Step-by-Step Guide to Completing the Debt Snowball Worksheet

The Debt Snowball Worksheet guides users through listing debts, calculating interest rates, and tracking progress. It simplifies the process of organizing payments and staying committed to debt repayment goals.

4.1 Listing Debts in Order of Payoff Balance

Begin by listing all debts, starting with the smallest payoff balance to the largest, regardless of interest rates. This approach provides quick victories, boosting motivation. Include each debt’s balance, minimum payment, and due date. Organizing debts this way helps users focus on eliminating smaller obligations first, creating a sense of progress that fuels continued effort in debt repayment.

4.2 Calculating Interest Rates and Monthly Payments

Next, calculate each debt’s interest rate and monthly payment. Input the principal amount, interest rate, and loan term into a calculator to determine the monthly payment. Record these figures in your worksheet. This step ensures accurate budget allocation and helps prioritize payments effectively, allowing users to understand the total interest paid over time and plan accordingly.

4.3 Tracking Progress and Adjustments

Regularly update your worksheet to reflect payments made and balances reduced. Celebrate milestones, like paying off a debt, to stay motivated. Adjust your budget or payment amounts as needed to accelerate progress. Tracking progress visually helps maintain focus and ensures long-term success in achieving financial freedom through the debt snowball method.

Case Studies and Real-Life Examples

Individuals share inspiring stories of paying off thousands in debt using the Debt Snowball Worksheet, highlighting how its structured approach leads to financial freedom and a sense of accomplishment.

5.1 Success Stories from Using the Debt Snowball Method

Many individuals have shared their success stories, revealing how the Debt Snowball Method helped them pay off significant amounts of debt. One user, for instance, managed to eliminate over $10,000 in credit card debt with a high interest rate of 29% by following the structured approach of the Debt Snowball Worksheet. This method not only provided a clear roadmap but also kept them motivated through quick wins, such as paying off smaller balances first. The sense of accomplishment from these early victories helped build momentum, leading to greater financial discipline and eventual freedom from debt. The psychological benefits of this approach were as impactful as the financial ones, demonstrating how the Debt Snowball Method can transform one’s relationship with money. By using the Debt Snowball Worksheet, individuals were able to organize their debts, calculate interest rates, and track their progress effectively. This tool became an essential part of their journey toward becoming debt-free, proving that with the right strategy and commitment, overcoming financial challenges is achievable. The success stories highlight the effectiveness of the Debt Snowball Method in creating a sustainable plan for debt repayment, making it a preferred choice for many who seek to regain control of their finances. The structured yet flexible nature of the method allowed individuals to stay on track, even when faced with unexpected expenses or setbacks. Overall, these testimonials underscore the power of the Debt Snowball Method in helping people achieve their financial goals and improve their overall well-being.

5;2 How the Worksheet Helped Individuals Pay Off Debt

The Debt Snowball Worksheet provided a clear, structured approach for individuals to organize and prioritize their debts. By listing debts, calculating interest rates, and tracking progress, users gained visibility and control over their financial obligations. The worksheet also helped automate monthly payments and facilitated communication with creditors for better terms. This tool empowered individuals to stay motivated and focused, ensuring steady progress toward becoming debt-free.

Comparing Debt Snowball and Debt Avalanche Methods

The Debt Snowball focuses on paying off smaller debts first for quick wins, while the Debt Avalanche prioritizes high-interest debt to minimize total interest paid.

6.1 Key Differences Between the Two Strategies

The Debt Snowball Method prioritizes paying off debts with the smallest balances first to create momentum, while the Debt Avalanche focuses on eliminating high-interest debt first to save money on interest over time. The Snowball emphasizes psychological wins, whereas the Avalanche targets financial efficiency, making each strategy suitable for different financial and personal preferences.

6.2 Which Method is More Effective for Faster Debt Repayment?

The Debt Avalanche often leads to faster debt repayment by reducing high-interest debt first, saving money on interest. However, the Debt Snowball’s quick wins can enhance motivation, potentially leading to consistent payments. The choice depends on whether financial efficiency or psychological momentum is more important for the individual’s debt repayment journey and success.

Common Questions About the Debt Snowball Worksheet

Users often ask why debts are listed by payoff balance and when to sell items. These questions highlight key strategies for maximizing the worksheet’s effectiveness.

7.1 Why List Debts by Payoff Balance Instead of Interest Rate?

The Debt Snowball Method prioritizes debts by payoff balance to create quick wins, boosting motivation. While higher-interest debt might seem logical, achieving smaller victories builds momentum and keeps individuals committed to their repayment journey. This approach aligns with psychological principles, emphasizing progress over pure financial optimization, which is a key factor in long-term success for many users.

7.2 When to Sell Items to Pay Off Debt

Selling items to pay off debt is advisable when it accelerates repayment without jeopardizing financial stability. High-interest debts, like credit cards, should be prioritized. Evaluate if selling non-essential assets can significantly reduce debt, then allocate proceeds strategically. This approach aligns with the Debt Snowball Method’s focus on quick wins and maintaining momentum in the repayment process effectively.

Practical Tips for Maximizing the Debt Snowball Worksheet

Use automation for consistent payments and track progress visually. Communicate with creditors to negotiate better terms, enhancing your debt repayment strategy effectively.

8.1 Automating Monthly Payments

Automating monthly payments ensures consistency and avoids late fees. Set up automatic transfers for each debt, aligning with your budget. Allocate a fixed portion of your income toward debt repayment to maintain discipline. Regularly review and adjust automated payments to reflect changes in income or expenses, optimizing your debt repayment progress. This approach simplifies the process and helps stay on track with the debt snowball method.

Proactively engaging with creditors can lead to more favorable repayment terms. Negotiate lower interest rates or temporary payment reductions to ease financial strain. Clearly explain your situation and commitment to debt repayment. Some creditors may offer hardship programs or balance transfer options, which can accelerate your progress. Regular communication fosters trust and may result in more flexible agreements. Common errors include ignoring emergency funds and overlooking high-interest debt, which can derail progress. Stay vigilant and adjust strategies to maintain financial stability and focus. Neglecting emergency funds can lead to financial setbacks, as unexpected expenses may force further borrowing. Prioritizing a small emergency fund ensures stability while paying off debt, preventing debt cycles. This step is crucial for maintaining consistent progress without financial strain or relapse into debt. Always allocate a portion of income to an easily accessible savings account. Ignoring high-interest debt can lead to paying significantly more over time, as interest accrues rapidly. Failing to address high-interest loans or credit cards first may prolong repayment and increase total costs. While the debt snowball method focuses on quick wins, combining it with a strategy to tackle high-interest debt can optimize savings and reduce financial burden more effectively. Budgeting is essential for organizing finances and ensuring consistent debt repayment. It helps allocate income toward expenses, savings, and debt, maintaining focus and discipline throughout the process. A spending plan is crucial for effective budgeting. It involves categorizing expenses into essentials and non-essentials, setting limits, and prioritizing debt repayment. By tracking income and expenses, individuals can allocate resources efficiently, ensuring consistent payments and building savings. This structured approach helps maintain financial discipline and aligns with the debt snowball method’s goal of achieving debt freedom. Regular reviews and adjustments are necessary to stay on track. Allocating income involves dividing it into three categories: essential expenses, savings, and debt repayment. Essential expenses include rent, utilities, and groceries, while savings should cover emergencies. The remaining income is dedicated to paying off debts, starting with the smallest balances. This structured approach ensures consistent progress toward debt freedom while maintaining financial stability. Extra funds can be used to accelerate debt repayment. Selling items to pay off debt can provide a quick influx of cash to accelerate repayment, helping reduce the overall debt burden more efficiently. When deciding what to sell to pay off debt, prioritize items that are no longer needed or used, such as unused electronics, furniture, or clothing. Consider selling high-value items that can generate significant cash quickly. Avoid selling sentimental or essential items unless necessary. Use the proceeds strategically to tackle smaller debts first, aligning with the debt snowball method to build momentum and stay motivated. Apply the proceeds from sold items directly toward your smallest debts to accelerate repayment. This approach aligns with the debt snowball method, providing quick wins that boost motivation. Allocate funds strategically, focusing on high-priority debts to eliminate them faster. Tracking progress with a debt snowball worksheet helps visualize the impact of these payments and keeps you committed to your financial goals. Regularly updating your debt snowball worksheet helps visualize progress, reinforcing motivation to continue. Celebrate milestones to maintain enthusiasm and commitment to your debt repayment journey. Visual tools like charts, graphs, and progress bars in the debt snowball worksheet help track repayment milestones. These visuals provide a clear picture of remaining balances and paid-off amounts, Celebrating milestones, like paying off a credit card or reaching a savings goal, boosts motivation and reinforces progress. Acknowledging these achievements, no matter how small, helps maintain commitment to the debt repayment journey. Whether it’s a small treat or sharing success with others, recognizing milestones keeps the process positive and encourages continued effort toward financial freedom. The Debt Snowball Method provides psychological benefits by offering quick wins, which build confidence and motivation. Paying off smaller debts first creates a sense of accomplishment, reinforcing the journey toward financial freedom and emotional relief from debt burdens. The Debt Snowball Method gains momentum by prioritizing smaller debts, allowing for quick victories. This approach fosters motivation as individuals see progress, which strengthens commitment and encourages continued effort. The psychological boost from each payoff propels users forward, making the journey feel manageable and reinforcing the effectiveness of the strategy. Emotional barriers, such as feelings of overwhelm or guilt, often hinder debt repayment progress. The Debt Snowball Method helps alleviate these by focusing on achievable milestones. Celebrating small victories builds confidence and reduces stress, making the process feel less daunting. This approach encourages persistence and helps individuals stay motivated, even when faced with emotional challenges. Explore budgeting tools, recommended reading, and podcasts for enhanced financial literacy. These resources supplement the Debt Snowball Method, offering practical advice and support for debt repayment success. Effective budgeting tools like Excel spreadsheets or apps such as Mint and You Need A Budget (YNAB) can streamline your financial planning. These tools help track expenses, categorize spending, and automate payments. For the Debt Snowball Method, they provide clear visuals of your progress, making it easier to stay motivated and aligned with your debt repayment goals. Consistency is key to long-term success. For deeper insights, explore books like The Total Money Makeover by Dave Ramsey, which aligns with the Debt Snowball strategy. Podcasts such as The Dave Ramsey Show and Planet Money offer practical advice and success stories. These resources provide motivation and strategies to complement your Debt Snowball Worksheet, helping you stay informed and inspired throughout your debt repayment journey. Using the Debt Snowball Worksheet provides a clear path to debt repayment, builds confidence, and helps achieve financial freedom through your steadfast commitment and effort. The Debt Snowball Worksheet is a powerful tool for organizing and tackling debt, offering a clear path to financial freedom. By focusing on quick wins and maintaining discipline, individuals can achieve lasting results. Staying committed to the process and celebrating milestones will keep motivation high, ensuring success in becoming debt-free. Remaining committed to debt repayment requires persistence and resilience. Each payment brings you closer to financial freedom, and celebrating small victories along the way can boost motivation. Surround yourself with supportive resources and remember, the journey may be challenging, but the rewards of a debt-free life are well worth the effort and dedication.8.2 Communicating with Creditors for Better Terms

Avoiding Common Mistakes When Using the Worksheet

9.1 Ignoring Emergency Funds

9.2 Overlooking High-Interest Debt

The Role of Budgeting in the Debt Snowball Strategy

10.1 Creating a Spending Plan

10.2 Allocating Income Toward Expenses, Savings, and Debt Repayment

Selling Items to Pay Off Debt

11.1 Deciding What to Sell

11.2 Using Proceeds to Accelerate Debt Repayment

Tracking Progress and Staying Motivated

12.1 Visual Tools for Monitoring Debt Repayment

making it easier to stay motivated. Incorporating these elements into your worksheet allows you to celebrate small victories, reinforcing your commitment to becoming debt-free.12.2 Celebrating Milestones

The Psychological Impact of the Debt Snowball Method

13.1 Building Momentum Through Quick Wins

13.2 Overcoming Emotional Barriers to Debt Repayment

Additional Resources for Debt Repayment

14.1 Recommended Budgeting Tools

14.2 Suggested Reading and Podcasts

15.1 Final Thoughts on Using the Debt Snowball Worksheet

15.2 Encouragement for Staying Committed to Debt Repayment

Leave a Comment